Tweet

Tweet

File Name: UltimateOscillator.efs

Description:

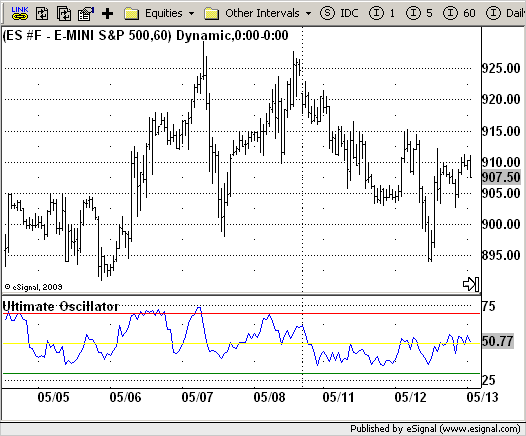

Ultimate Oscillator

Formula Parameters:

Short Period : 7

Med Period : 14

Long Period : 28

Notes:

Oscillators typically compare a security's smoothed price with its

price x-periods ago. Larry Williams noted that the value of this type

of oscillator can vary greatly depending on the number of time periods

used during the calculation. Thus, he developed the Ultimate Oscillator

that uses weighted sums of three oscillators, each of which uses a different

time period.

The three oscillators are based on Williams' definitions of buying and

selling "pressure".

Download File:

UltimateOscillator.efs

EFS Code:

Description:

Ultimate Oscillator

Formula Parameters:

Short Period : 7

Med Period : 14

Long Period : 28

Notes:

Oscillators typically compare a security's smoothed price with its

price x-periods ago. Larry Williams noted that the value of this type

of oscillator can vary greatly depending on the number of time periods

used during the calculation. Thus, he developed the Ultimate Oscillator

that uses weighted sums of three oscillators, each of which uses a different

time period.

The three oscillators are based on Williams' definitions of buying and

selling "pressure".

Download File:

UltimateOscillator.efs

EFS Code:

PHP Code:

/*********************************

Provided By:

eSignal (Copyright c eSignal), a division of Interactive Data

Corporation. 2009. All rights reserved. This sample eSignal

Formula Script (EFS) is for educational purposes only and may be

modified and saved under a new file name. eSignal is not responsible

for the functionality once modified. eSignal reserves the right

to modify and overwrite this EFS file with each new release.

Description:

Ultimate Oscillator

Version: 1.0 05/08/2009

Formula Parameters: Default:

Short Period 7

Med Period 14

Long Period 28

Notes:

Oscillators typically compare a security's smoothed price with its

price x-periods ago. Larry Williams noted that the value of this type

of oscillator can vary greatly depending on the number of time periods

used during the calculation. Thus, he developed the Ultimate Oscillator

that uses weighted sums of three oscillators, each of which uses a different

time period.

The three oscillators are based on Williams' definitions of buying and

selling "pressure."

**********************************/

var fpArray = new Array();

var bInit = false;

function preMain() {

setStudyTitle("Ultimate Oscillator");

setCursorLabelName("UO");

addBand(70, PS_SOLID, 1, Color.red);

addBand(50, PS_SOLID, 1, Color.yellow);

addBand(30, PS_SOLID, 1, Color.green);

setStudyMax(80);

setStudyMin(20);

var x = 0;

fpArray[x] = new FunctionParameter("Period_short", FunctionParameter.NUMBER);

with(fpArray[x++]) {

setName("Short Period");

setLowerLimit(1);

setDefault(7);

}

fpArray[x] = new FunctionParameter("Period_med", FunctionParameter.NUMBER);

with(fpArray[x++]) {

setName("Med. Period");

setLowerLimit(1);

setDefault(14);

}

fpArray[x] = new FunctionParameter("Period_long", FunctionParameter.NUMBER);

with(fpArray[x++]) {

setName("Long Period");

setLowerLimit(1);

setDefault(28);

}

}

var xUO = null;

function main(Period_short, Period_med, Period_long){

var nBarState = getBarState();

if (nBarState == BARSTATE_ALLBARS) {

if (Period_short == null) Period_short = 7;

if (Period_med == null) Period_med = 14;

if (Period_long == null) Period_long = 28;

}

if (bInit == false) {

xUO = efsInternal("Calc_UO", Period_short, Period_med, Period_long);

bInit = true;

}

nUO = xUO.getValue(0);

if (nUO == null) return;

return nUO;

}

var xMA1TL = null;

var xMA2TL = null;

var xMA3TL = null;

var xMA1TR = null;

var xMA2TR = null;

var xMA3TR = null;

var xTL = null;

var xTR = null;

var bSecondInit = false;

function Calc_UO(Period_short, Period_med, Period_long) {

var nMA1TL = 0;

var nMA2TL = 0;

var nMA3TL = 0;

var nMA1TR = 0;

var nMA2TR = 0;

var nMA3TR = 0;

var nRes = 0;

if (bSecondInit == false) {

xTL = efsInternal("Calc_TrueLow");

xMA1TL = sma(Period_short, xTL);

xMA2TL = sma(Period_med, xTL);

xMA3TL = sma(Period_long, xTL);

xTR = atr(1);

xMA1TR = sma(Period_short, xTR);

xMA2TR = sma(Period_med, xTR);

xMA3TR = sma(Period_long, xTR);

bSecondInit = true;

}

nMA1TL = xMA1TL.getValue(0);

nMA2TL = xMA2TL.getValue(0);

nMA3TL = xMA3TL.getValue(0);

nMA1TR = xMA1TR.getValue(0);

nMA2TR = xMA2TR.getValue(0);

nMA3TR = xMA3TR.getValue(0);

if (nMA1TL == null || nMA2TL == null || nMA3TL == null) return;

nRes = (4 * nMA1TL / nMA1TR + 2 * nMA2TL / nMA2TR + nMA2TL / nMA2TR) / 7;

return nRes * 100;

}

function Calc_TrueLow() {

var nRes = 0;

var nClose1 = close(-1);

if (nClose1 == null) return;

nRes = Math.min(low(0), nClose1);

nRes = close(0) - nRes;

return nRes;

}