Tweet

Tweet

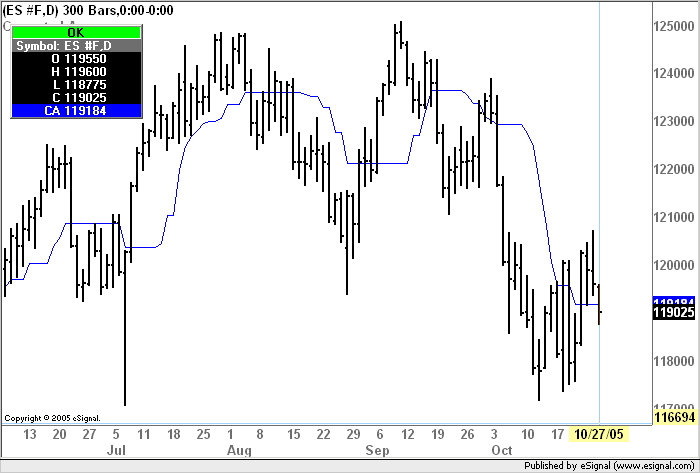

The following Code of a moving average is published in a bulletin board by Andreas Uhl.

I can´t "read" a Metastock Code. Is it possible to code this in eSignal efs?

Thank You!

Helmut

{Corrected Average (CA), A.Uhl, Oct. 25, 2005}

vars:

CA(0),SA(0),n(0),

v1(0),v2(0),K(0);

inputs:

Price(Close),length(35);

if CurrentBar=1 then

CA=Price

else

begin

if CurrentBar<length then

n=CurrentBar

else

n=length;

SA=Average(Price,n);

v1=Square(StdDev(Price,n));

v2=Square(CA[1]-SA);

if v2<v1 then

K=0

else

K=1-v1/v2;

CA=CA[1]+K*(SA-CA[1]);

end;

Plot1(CA,"Corrected Average",Red,White,3);

Plot2(SA,"Simple Average",Blue,White,1);

I can´t "read" a Metastock Code. Is it possible to code this in eSignal efs?

Thank You!

Helmut

{Corrected Average (CA), A.Uhl, Oct. 25, 2005}

vars:

CA(0),SA(0),n(0),

v1(0),v2(0),K(0);

inputs:

Price(Close),length(35);

if CurrentBar=1 then

CA=Price

else

begin

if CurrentBar<length then

n=CurrentBar

else

n=length;

SA=Average(Price,n);

v1=Square(StdDev(Price,n));

v2=Square(CA[1]-SA);

if v2<v1 then

K=0

else

K=1-v1/v2;

CA=CA[1]+K*(SA-CA[1]);

end;

Plot1(CA,"Corrected Average",Red,White,3);

Plot2(SA,"Simple Average",Blue,White,1);

Attached Files

Comment