Its normal to have a 7 to 15 point difference when the change over happens. What I do is when it changes is change symbols to the actual contract for a few weeks until the contract establishes a range. Try using ES H7 it will help define the charts better as far as S/R and so on.

Then just flip back in a few weeks. Just another thing you have to account for when trading futures.

billnc

The enclosed excerpt from an article by Bob Fulks briefly explains the reason for the difference in prices at rollover between futures contracts. Note that at the time the article was published the S&P price, interest rate and dividend rate were relatively similar to today's hence the similarity in the increase in the premium

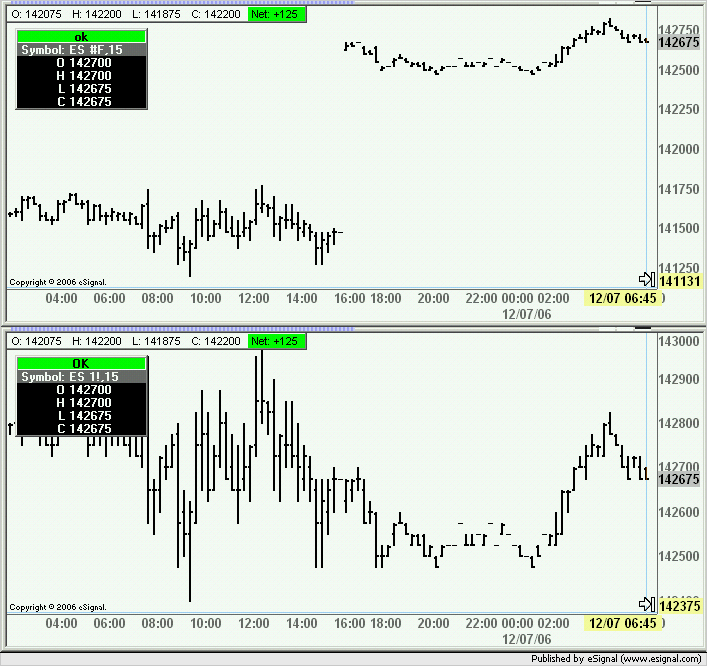

One way to resolve this difference is to create your own continuous contract using the Continuous Contract Settings tool and back adjust the contracts. In the image enclosed below you can see two charts one for ES #F and the other for ES 1! set to back adjust the prior contracts.

For instructions on how to configure a user defined continuous contract see this article in the eSignal KnowledgeBase

Alex

from Back-Adjusting Futures Contracts by Bob Fulks March 2000 The pricing of a futures contract is slightly different than the price of the underlying commodity since it includes other factors. This difference is called the "premium". For the S&P Futures this difference includes the cost of interest and the dividends of the S&P stocks.

The theoretical value is called the "fair value". It is the price at which investing in the underlying commodity has the same return as investing in the futures contract. For the S&P futures it is calculated as follows:

Futures_Price = Cash_Price * (1 + d * (i - v) / 365)

where:

i = interest rate for fair value calculation = about 5% now

v = dividend rate of the S&P cash index = about 1% now

d = days_to_expiration

At rollover, the days_to_expiration number jumps, causing the jump in the premium. With today's values, the jump in price is about 1%, or about 12 points on the S&P futures contract [the actual number does depend upon the level of the index, interest and dividend rates].

Tweet

Tweet

Comment